The Backdoor Roth IRA: How I Legally Funded a Roth Even Though I Earn Too Much

Prefer video? Watch the short version on Instagram →

"You earn too much for a Roth IRA."

That sentence is technically true and completely beatable. If your income is above the 2026 Roth limits, the front door is locked — but there's a side door the IRS has explicitly allowed since 2010. I walked through it this year for $7,500 inside Fidelity, and I'm going to show you every click, including the one gotcha that breaks the whole thing if you miss it.

This is the move high earners use to fund a Roth anyway. It's called the Backdoor Roth IRA, and it's boringly legal.

Why the income cap exists (and why it's easy to sidestep)

A Roth IRA lets your money grow and come out completely tax-free in retirement. Because that deal is so good, the IRS caps who can contribute directly. For 2026, direct Roth contributions phase out here:

- Single filers: $153,000–$168,000 (partial), fully blocked above $168,000

- Married filing jointly: $242,000–$252,000 (partial), fully blocked above $252,000

Earn above the top number and you can't put a dollar into a Roth the normal way.

Here's the loophole. There's a separate rule for Roth conversions — moving money from a Traditional IRA into a Roth. That conversion used to have its own $100,000 income limit, but the Tax Increase Prevention and Reconciliation Act (TIPRA) of 2005 removed it, effective January 1, 2010. Since then, anyone at any income can convert. The Backdoor Roth just chains a contribution and a conversion together: put money in a Traditional IRA (allowed at any income), then convert it to Roth (also allowed at any income). Front door locked, side door wide open.

Step 1 — Bank → Fidelity Cash Management Account

Move $7,500 from your checking account into a Fidelity Cash Management Account. It's a plain ACH transfer — link your bank, enter the amount, submit.

Give it 2–3 business days to settle before the next step. Trying to move unsettled cash is the most common reason people get stuck on day one.

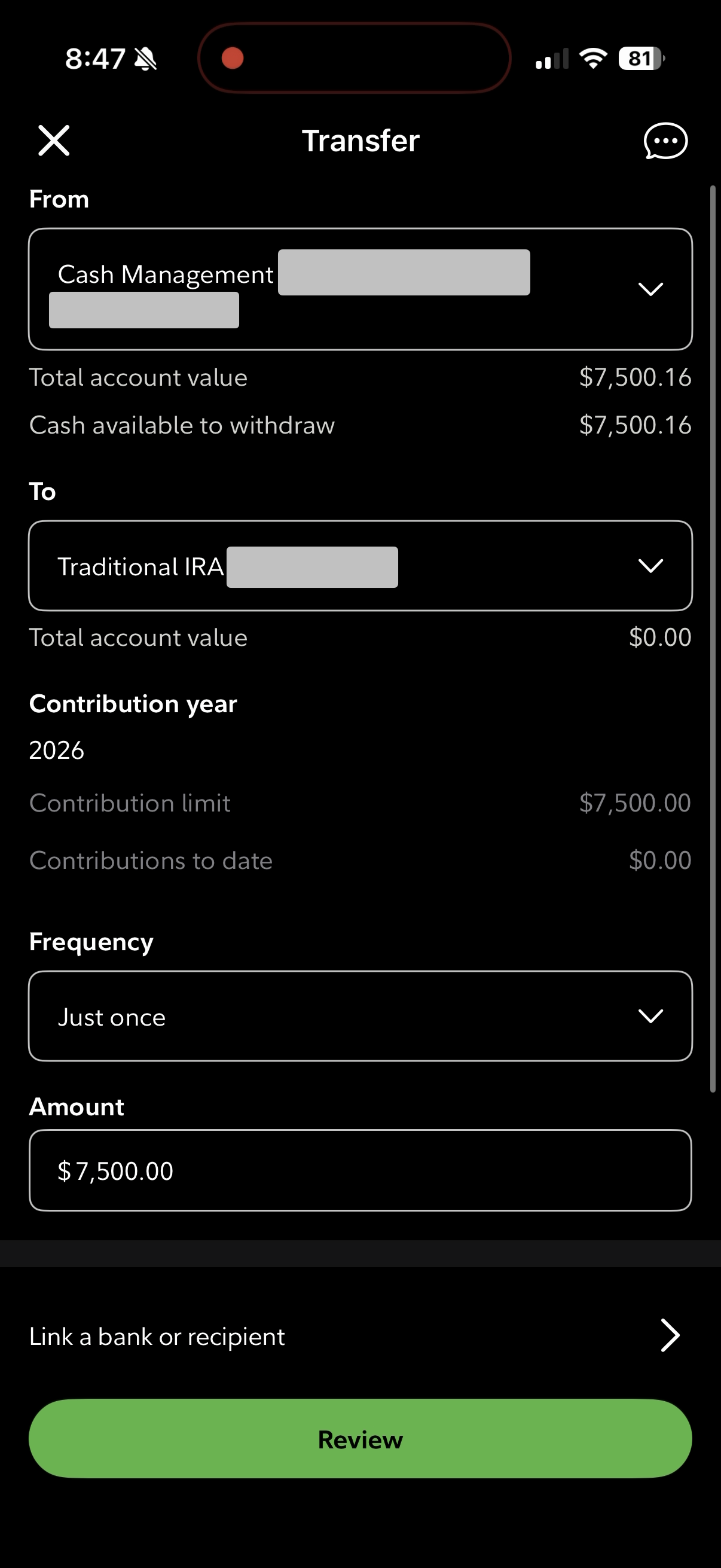

Step 2 — Cash Management → Traditional IRA

Push that $7,500 into a Traditional IRA as a non-deductible contribution. ($7,500 is the full 2026 IRA limit if you're under 50.)

"Non-deductible" is the point, not a mistake. Your income is too high to deduct it — so this money has already been taxed, which is exactly what makes the later conversion clean. At tax time you'll file IRS Form 8606 to record this as basis (after-tax money). That form is what stops you from being taxed twice on the same dollars later. Skip it and you'll overpay — keep every 8606 you ever file.

That $7,500 is now cash in your Traditional IRA. The next step is the conversion — and it's where the app quietly fails you.

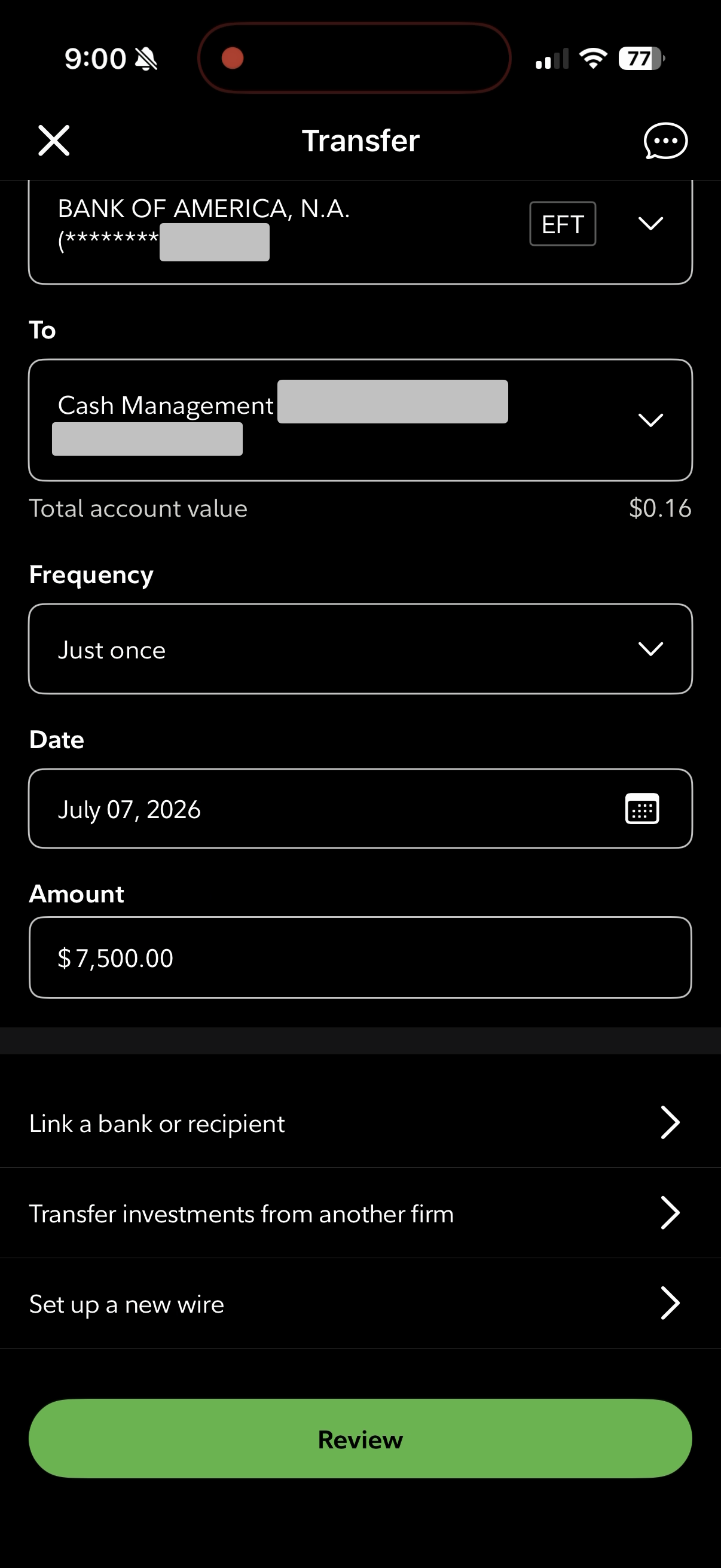

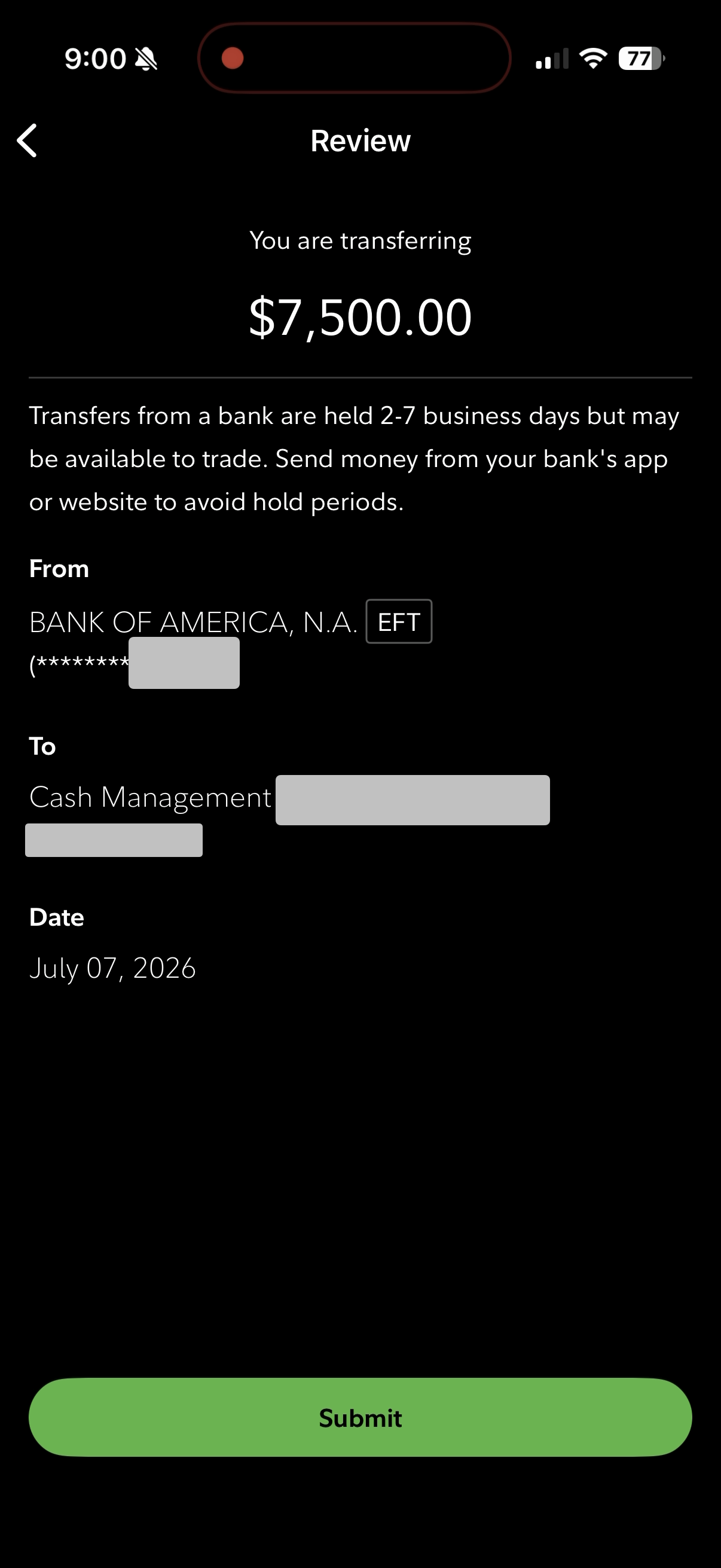

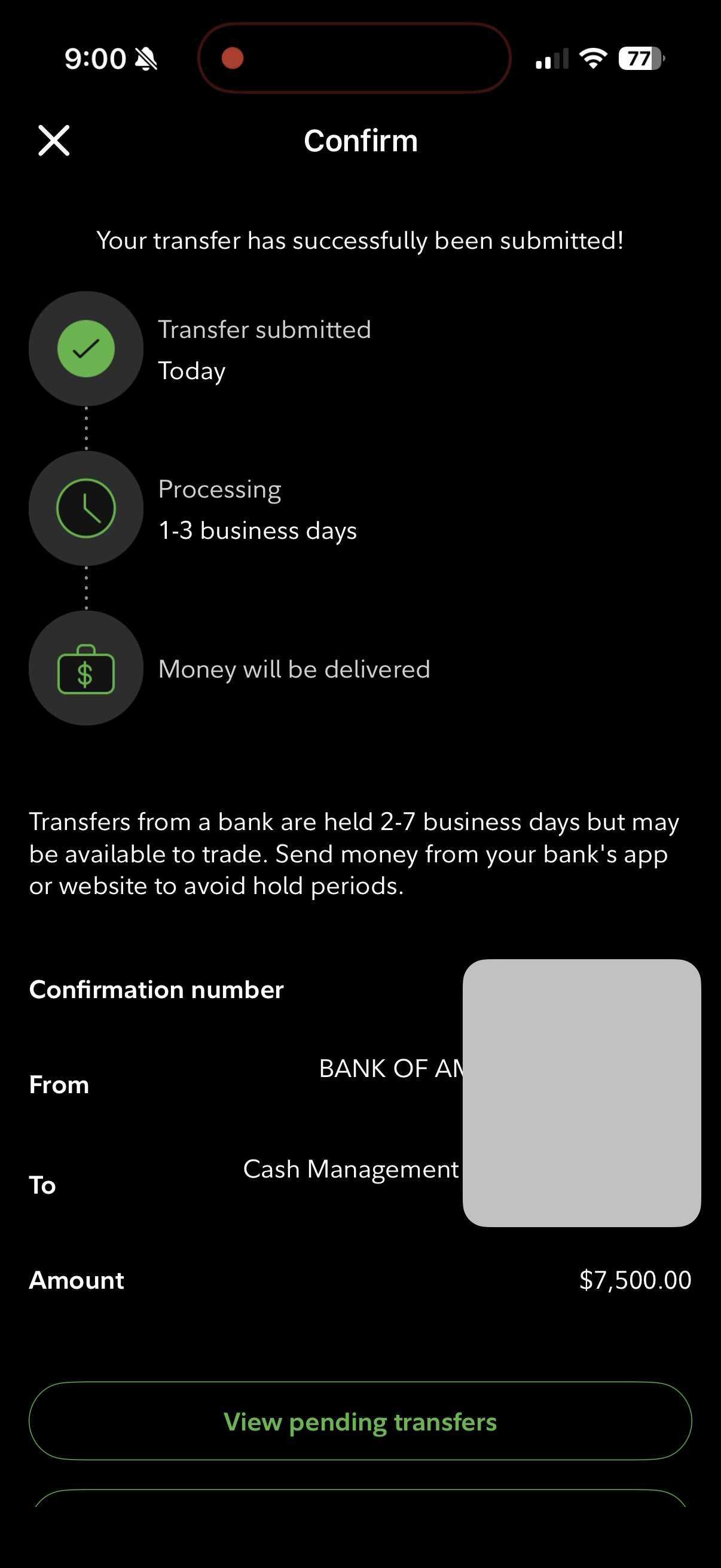

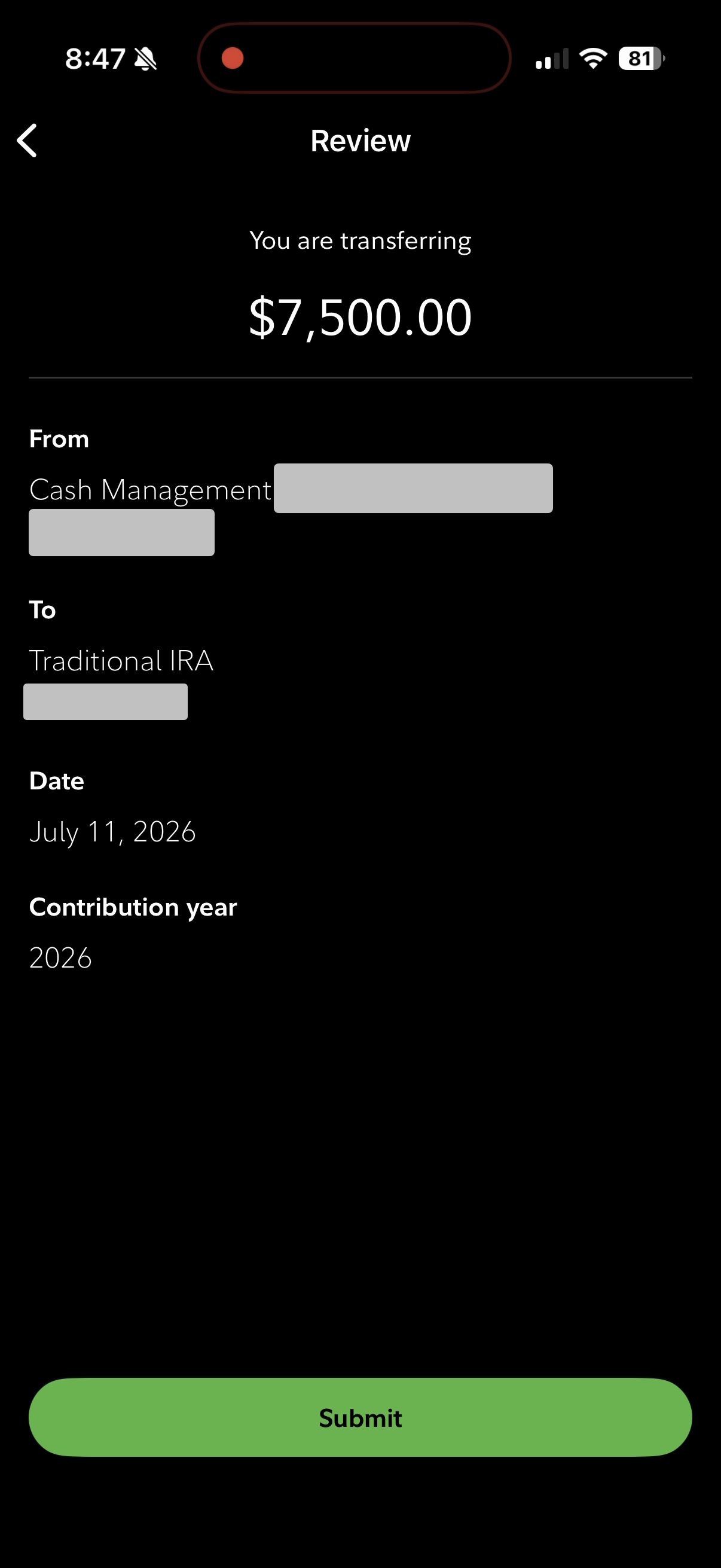

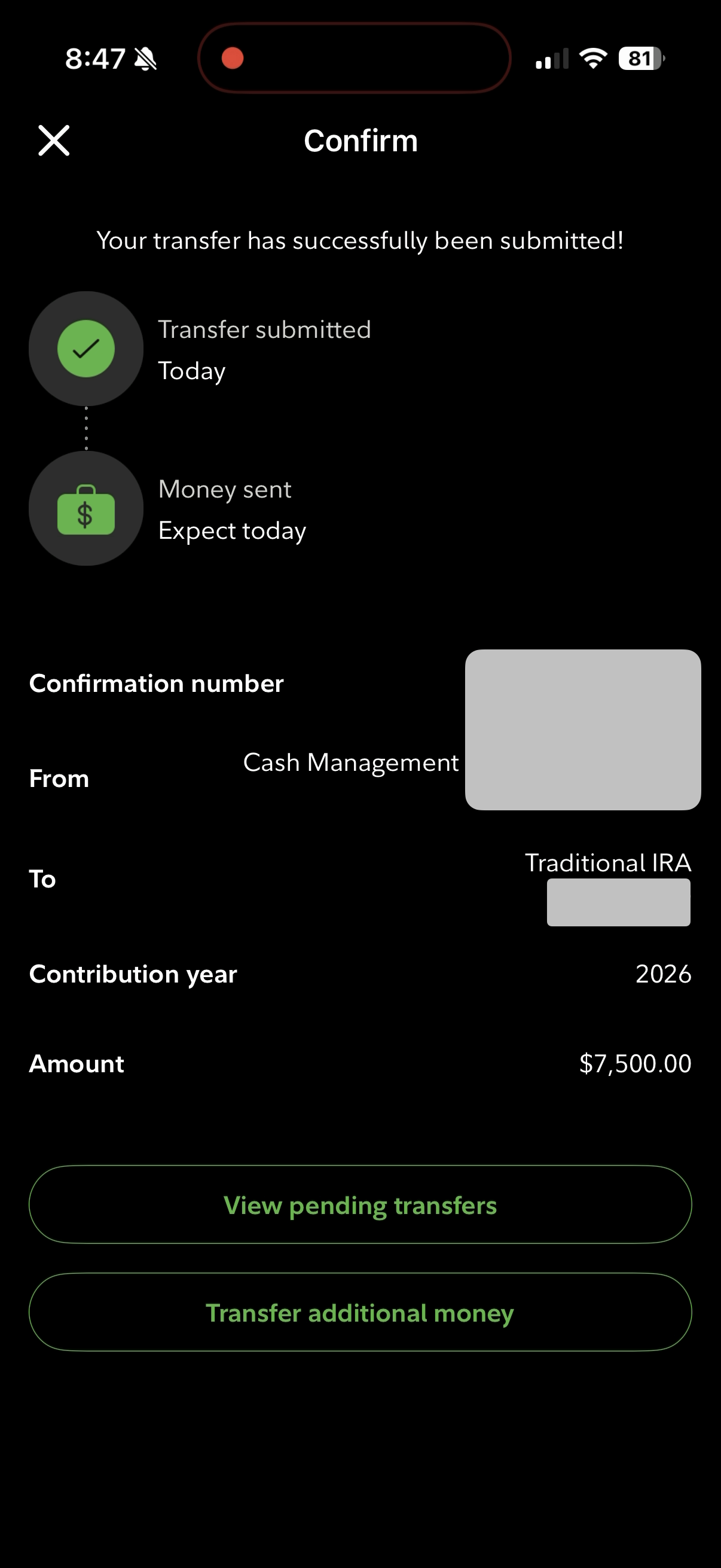

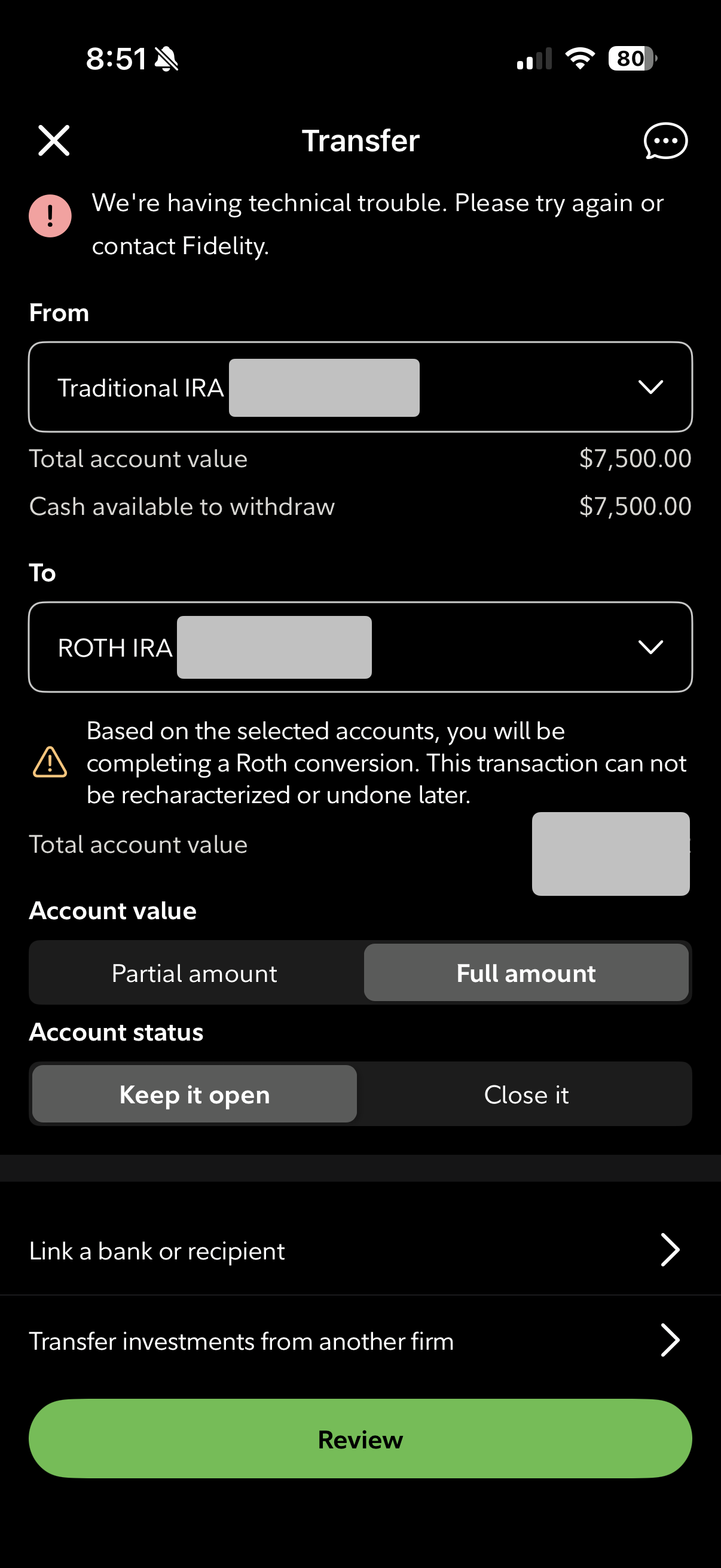

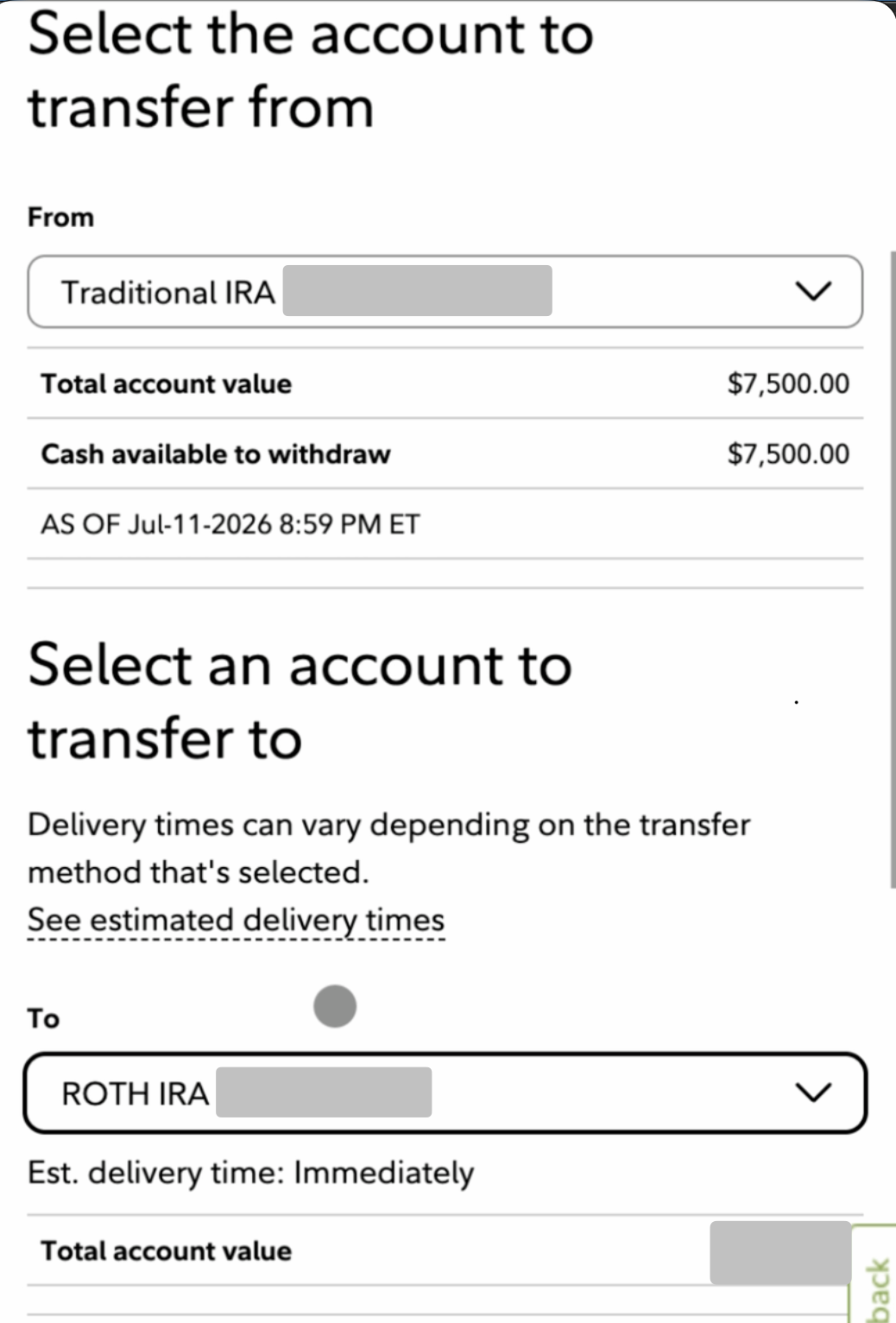

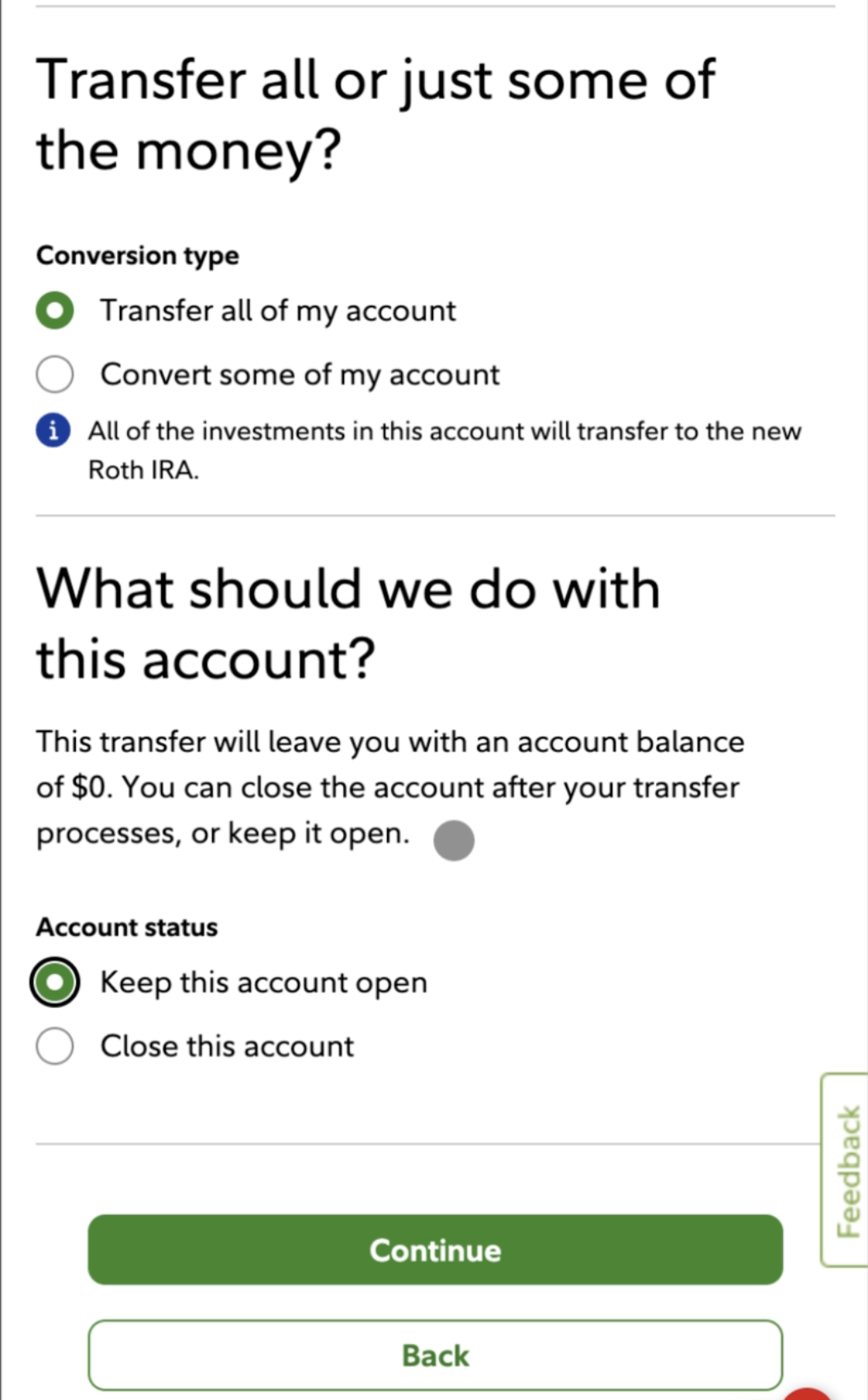

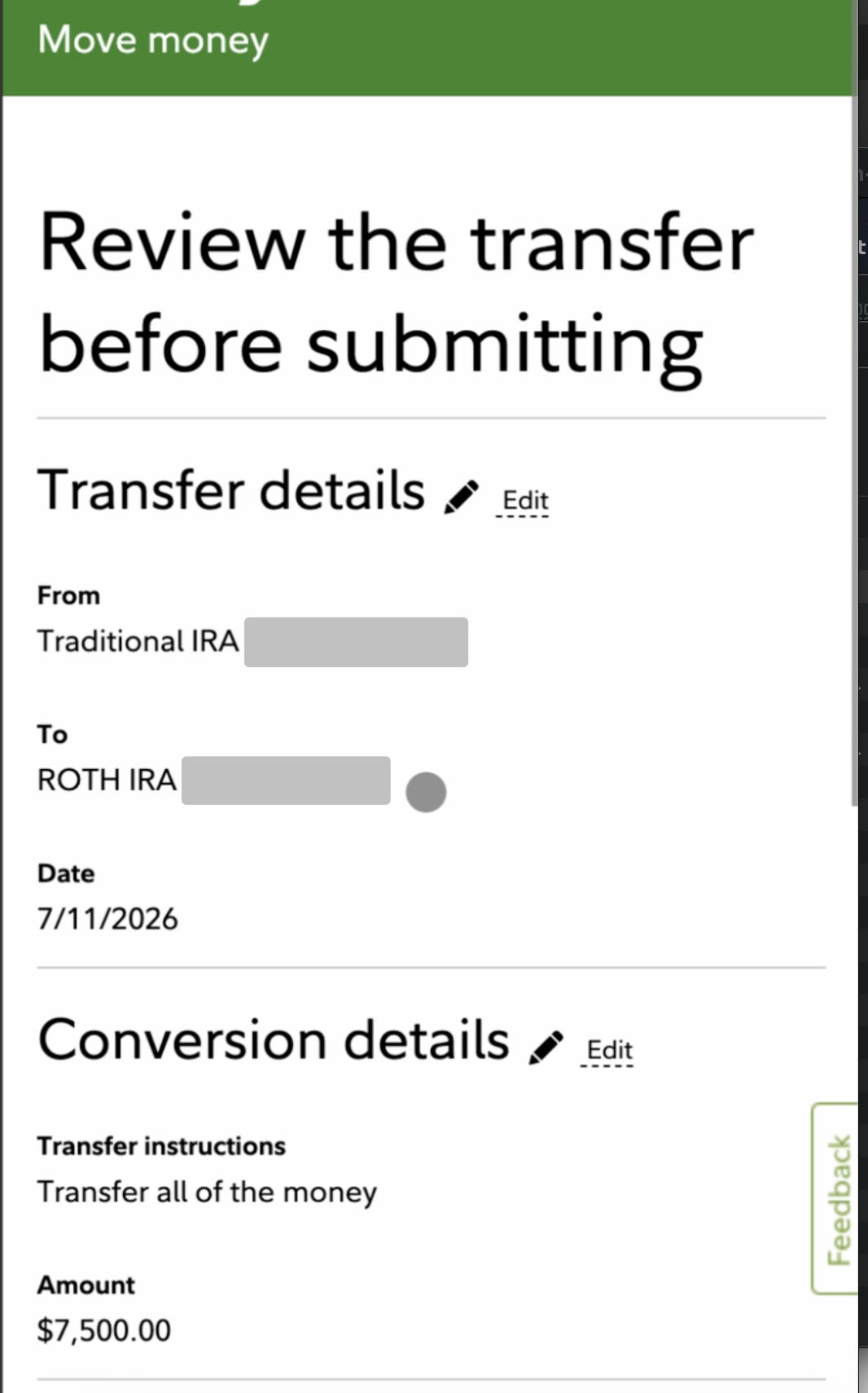

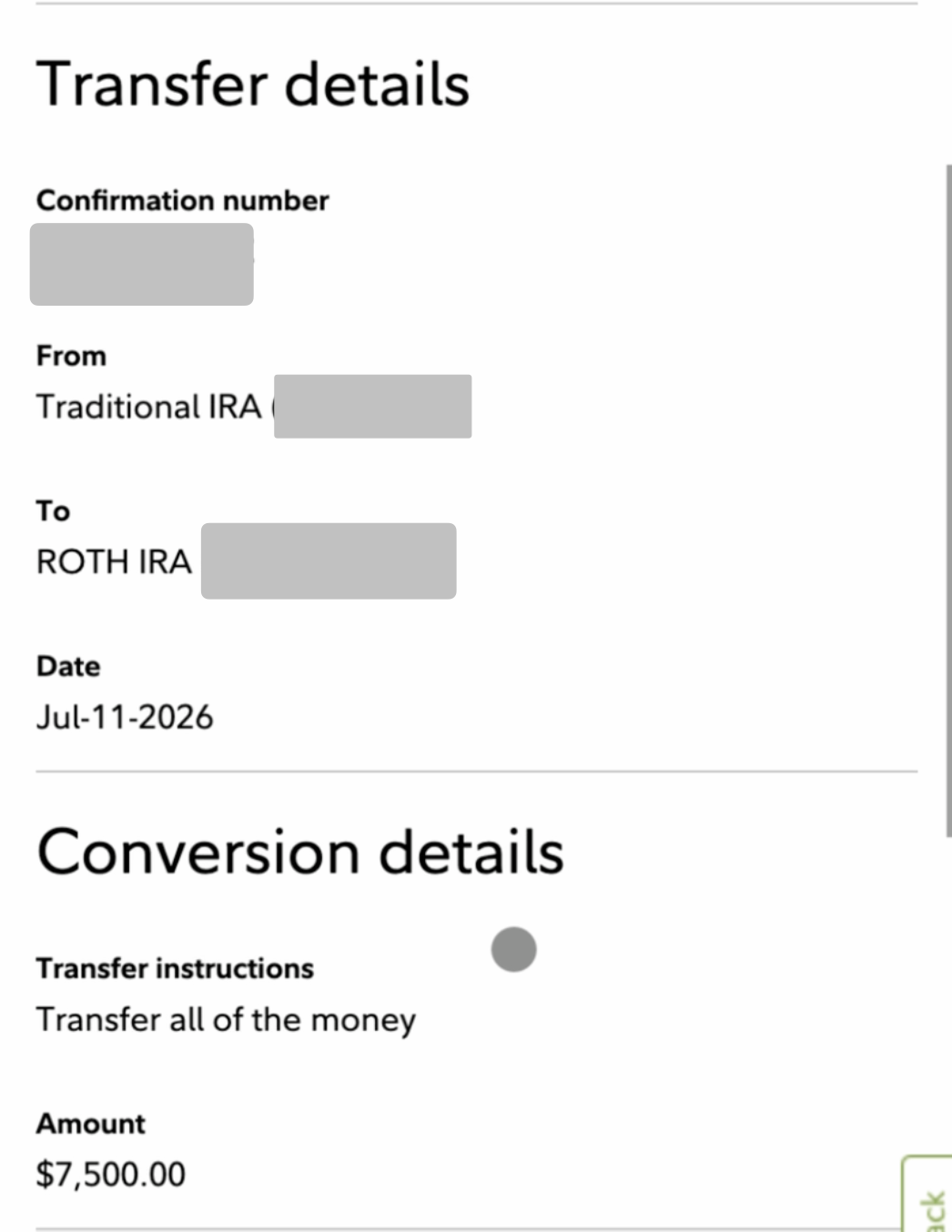

Step 3 — Traditional IRA → Roth IRA (the mobile-app gotcha)

Now convert the Traditional IRA to a Roth IRA. It's a one-click conversion — but here's the catch that wastes people an afternoon:

Fidelity's mobile app can't do it. The "Move Money" flow in the app errors out on a Roth conversion. You have to use fidelity.com on a desktop browser. On desktop it's a single confirmation.

Do the conversion the same day the contribution settles, or as close to it as you can. Why the rush? If the cash sits in the Traditional IRA and earns even a few dollars of gains before you convert, those gains are taxable at conversion. Convert fast and there's nothing to tax — you're moving $7,500 of already-taxed money straight into the Roth.

Step 4 — the step nobody talks about (INVEST it)

This is where most people quietly lose. They finish the conversion, see $7,500 in the Roth, and stop. Cash sitting in a Roth IRA does nothing. It's not invested — it's just parked, earning close to nothing, while you think you're building wealth.

You have to actually buy the fund. My picks, all S&P 500 index funds with rock-bottom fees:

- VOO (Vanguard S&P 500 ETF) — 0.03% expense ratio

- FXAIX (Fidelity 500 Index Fund) — 0.015% expense ratio

- SWPPX (Schwab S&P 500 Index) — 0.02% expense ratio

Pick one, buy $7,500 of it, done. The account is the wrapper; the fund is the engine. An empty Roth is a garage with no car in it.

The math nobody shows you

Here's why this one move is worth the 20 minutes and the Form 8606 headache.

- $7,500 once, left invested for 30 years at a 10% average return → about $131,000 — all tax-free.

- $7,500 every year for 30 years at 10% → roughly $1,230,000 — all tax-free.

Now compare that same $7,500/year to a regular taxable brokerage account. After tax drag along the way and long-term capital gains tax at withdrawal, you'd land around $860,000. Same contributions, same fund, same market — but roughly $370,000 less, purely because of the account you chose to hold it in.

That $370,000 is the cost of using the wrong wrapper. The Backdoor Roth is how high earners avoid paying it.

The pro-rata rule — the one landmine to avoid

Read this part twice. The Backdoor Roth works cleanly only if you have no other pre-tax IRA money on December 31 of the conversion year.

If you hold a balance in a Traditional IRA, SEP IRA, or SIMPLE IRA, the IRS applies the pro-rata rule: it treats all your IRA money as one pool and taxes a proportional slice of your conversion. Example — if you have $42,500 of pre-tax IRA money and add your $7,500 non-deductible contribution, only 15% of your conversion counts as after-tax. The rest gets taxed. The clean backdoor becomes a taxable mess.

The fix: roll any existing pre-tax IRA balances into your 401(k) before you do the Backdoor Roth. A 401(k) doesn't count in the pro-rata calculation, so this empties the pool and makes your conversion clean again. If you have old IRA money and you're not sure how to handle it, talk to a CPA before you convert — this is the single place people get burned, and it's expensive to unwind after year-end.

Who this ISN'T for

The Backdoor Roth is a specific tool for a specific person. Skip it if:

- You have existing pre-tax IRA balances you can't roll into a 401(k). Solve the pro-rata problem first, or the whole thing backfires.

- Your income is under the phase-out limits. Then you don't need the backdoor at all — just contribute to a Roth directly. Same destination, none of the steps.

- You haven't captured your full 401(k) match yet. That's free money and comes first — see Episode 2. Don't run the fancy move while leaving the guaranteed one on the table.

Order matters more than sophistication. The backdoor is step six or seven, not step one.

This is Episode 5 of the Paycheck Playbook. Back up one: Episode 4 — the emergency fund that protects everything else →. Episode 6 next week is the one fund I put everything into.

Comment "BACKDOOR" on the reel and I'll send you the Form 8606 walkthrough. Follow @joinforbonus for the full series, and subscribe below for the weekly blog — plain-English money, no hype.

Liked This Post?

Get more like it in your inbox

One short email a week. No spam, no upsells — ever.